Australia's Energy Commodity Resources 2024 Geothermal

Page last updated:15 July 2024

Geothermal

Summary statistics for geothermal, 2022.

| Production capacity | |

|

Electricity – | |

|

Direct use 94.4 MWth |

|

Exploration 112 tenements# ( 700% since 2021) |

|

Status Early stages of development |

Abbreviations:

MWth = Megawatts thermal.

Notes:

#exploration tenements in 2024 include 32 granted and 80 under application areas, up from a total of 14 in 2021.

Key messages

Key messages

- Geothermal energy is the Earth's natural internal heat and has been used for millennia. As a resource, it is used as a direct source of heat and to generate electricity. Electricity generation from geothermal energy is achieved via steam turbines and was pioneered more than 100 years ago.

- Geothermal energy resources represent one of the cleanest and most reliable commodities for energy generation. It has minimal wastes or pollutants and is essentially inexhaustible. Unlike most renewable energy resources, geothermal energy is not variable and does not require energy storage to provide a constant supply of electricity or heat.

- Significant uncertainties are associated with geothermal energy resources, unlike solar and wind resources. However, once a resource is defined it can provide a reliable, high-capacity baseload energy supply without requiring energy storage back-up.

- The geothermal gradient describes the rate of temperature increase with increasing depth beneath the Earth’s surface. Areas that have a high geothermal gradient are prime targets for the exploration of geothermal energy sources.

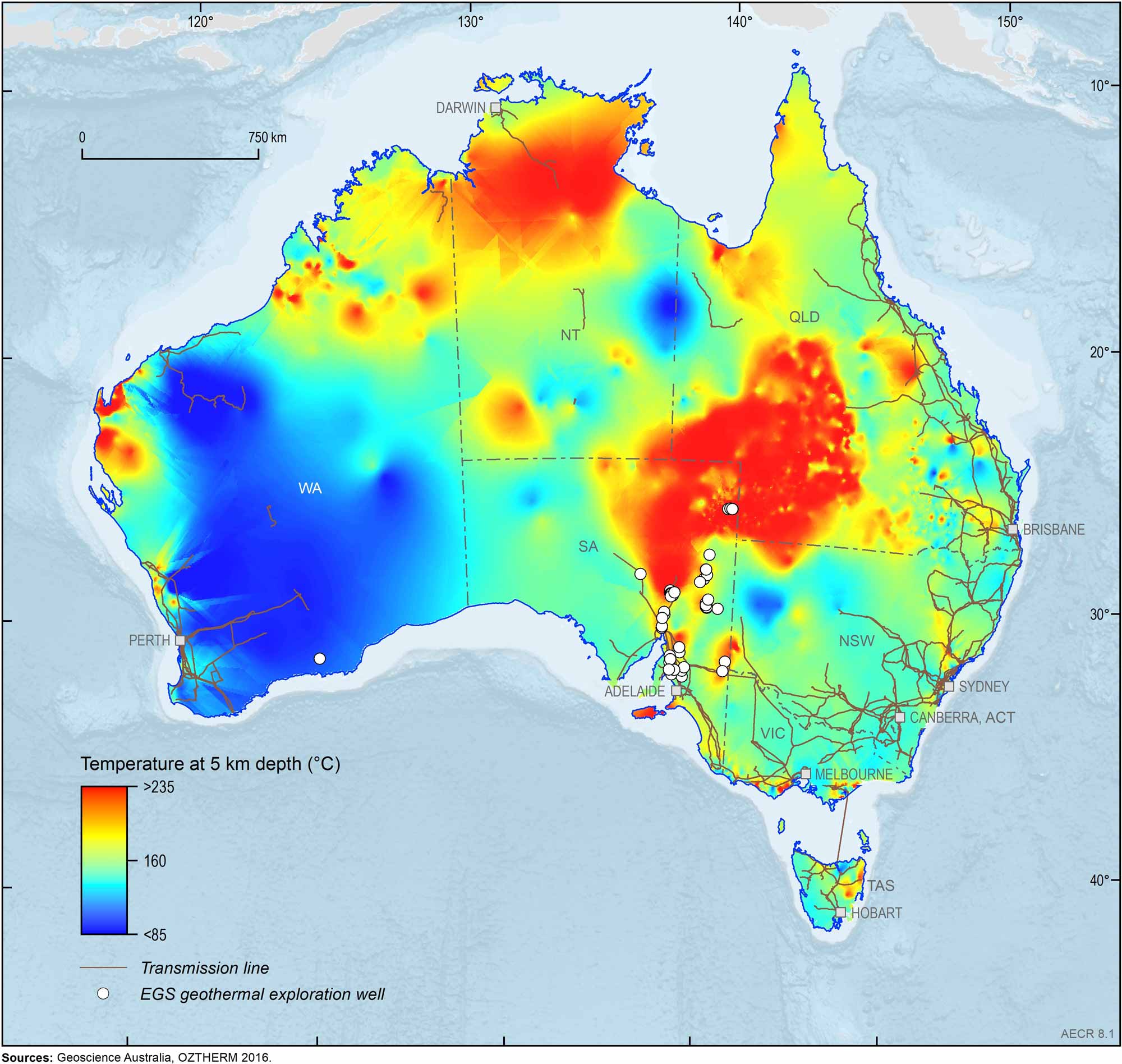

- Worldwide, most geothermal electricity is generated in regions where active volcanism creates high heat flows. Australia has no known active volcanism, and the heat source for Australia’s unconventional geothermal systems is a combination of radiogenic heat production from rocks in the upper crust and conducted heat from the mantle (Figure 8.1). An insulating layer of blanketing sediments is needed to allow heat to accumulate and high temperatures to be reached.

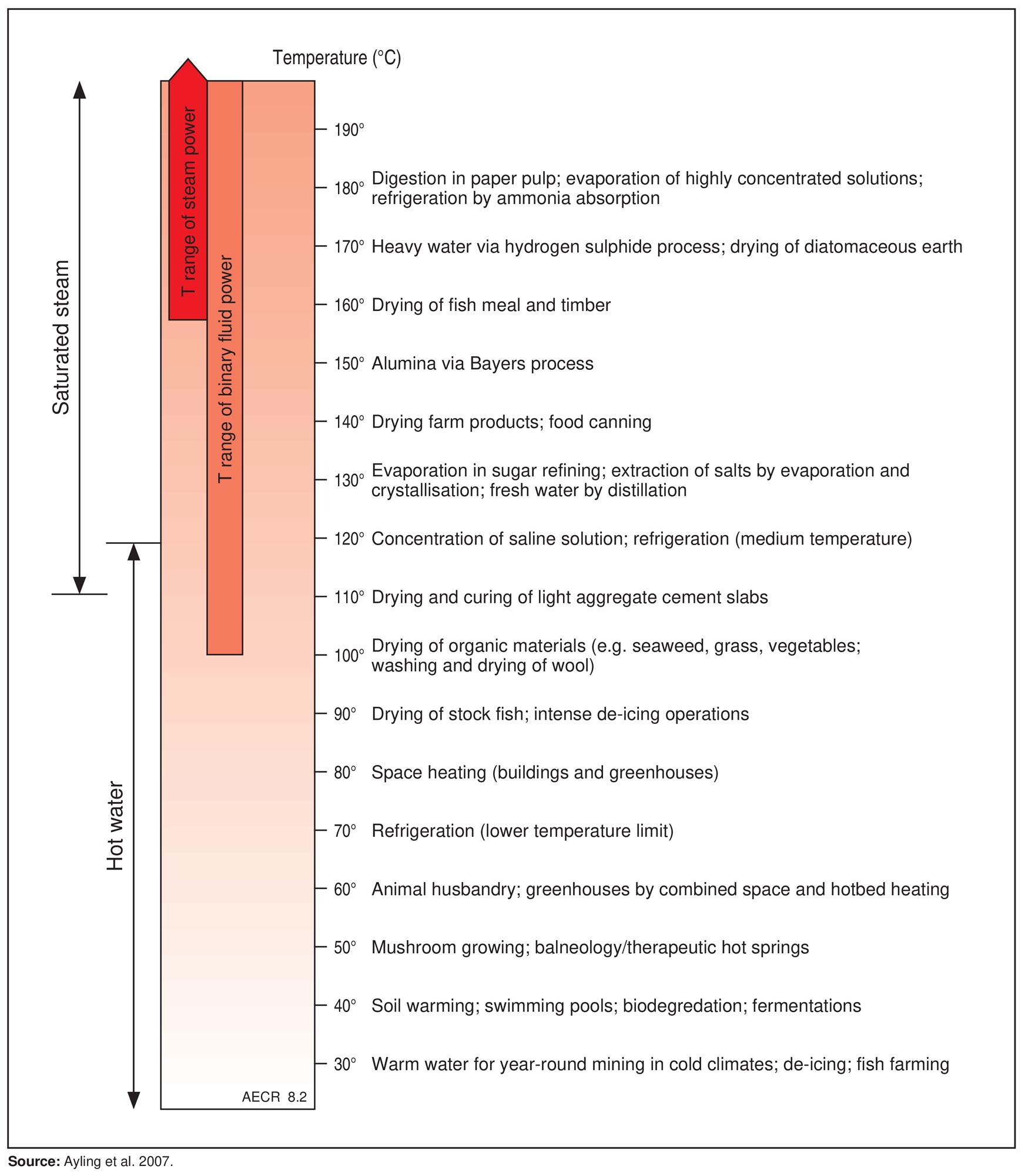

- In addition to electricity generation, technologies also exist to use geothermal heat for industrial and heating processes—such as drying and cooling and for spa baths—these are collectively called direct-use applications (Figure 8.2). Also, at depths of several metres beneath the land surface, the temperature is quite stable year-round, and a ground source heat pump (GSHP) can effectively heat and cool a building.

- Australian geothermal installations include many ground-source heat pumps, mostly installed in the colder regions of Australia, and numerous direct-use installations, largely located in the Perth, Otway, Gippsland and Great Artesian basins.

- The geothermal energy sector in Australia is still in its infancy. The development of geothermal energy for utility-scale electricity generation has recently experienced a resurgence of interest as evidenced by a substantial increase in permit applications across the country.

- Recent breakthroughs in geothermal technology have the potential to significantly impact on the future development of geothermal energy in Australia. These include improved efficiency in power generation technology (which reduces the minimum temperature required), breakthroughs in Enhanced Geothermal System technology and the rapidly developing sector of Advanced Geothermal Systems, which utilise closed loop technology that eliminates the need for permeable reservoirs.

Figure 8.1. Predicted temperature at 5 km depth and locations of geothermal exploration wells.

Figure 8.2. Direct-use applications of geothermal energy.

Australia’s resources

Australia’s resources

A successfully operating geothermal system has two key properties: elevated temperature, and the ability to pass water through hot rock to commercially move enough heat energy to the surface. Most geothermal power stations access temperatures of >160°C, at depths of 2 km beneath the surface.

As noted above, Australia has no active volcanoes, and generally has a lower geothermal gradient than regions with active conventional geothermal production. As a result, temperatures of >160°C are not reached until depths of 3 km across most of Australia. Australia’s geothermal resources are therefore considered to be unconventional and are classified as either an enhanced geothermal system (EGS) or a hot sedimentary aquifer (HSA).

Box 8.1 Conventional and unconventional geothermal systems

Geothermal energy resources can be classified into conventional and unconventional systems. Conventional geothermal systems are characterised by thermal, permeability and fluid properties that are favourable to the heat resource being extracted by drilling only. Conventional geothermal resources usually occur at depths <3 km. Unconventional geothermal systems have sufficient heat but lack the permeability and/or fluid for to achieve sustained fluid flow, and therefore require stimulation to extract heat. Unconventional geothermal systems occur over a range of depths, up to 7 km.

Australia’s unconventional geothermal resource potential is considerable, occurring in locations where key geological characteristics co-occur, including:

- widespread occurrence of basement rocks, especially granites, with unusually high heat-generating properties;

- regions of anomalously elevated heat flow from the Earth’s mantle beneath the upper crust; and

- regionally extensive sedimentary basins that are filled with thermally insulating sediments or volcanic rocks.

Hot sedimentary aquifers (HSA) are shallow (less than 3 km) and usually have good natural permeability, provided that the sediments have not undergone metamorphism. Deeper in the rocks, beneath insulating sedimentary basins, the crystalline basement rocks have poor permeability. For these basement rocks to be able to flow water they need to be fracture stimulated; these are called enhanced geothermal systems (EGS). Both EGS and HSA resources can be used for electricity generation or in direct-use applications. To be commercially viable, EGS and HSA resources would need to be able to produce electricity at a competitive cost over a sufficiently long timeframe to make a project financially viable. This metric is commonly derived by calculating the Levelised Cost of Energy (LCOE), which accounts for the total average cost of the energy over the project lifetime.

Hot sedimentary aquifer (HSA) resources

The HSA resource in Australia could be substantial, as sedimentary basins with effective aquifers cover most of the Australian continent. However, only a few basins are known to have high enough geothermal gradients for higher-temperature HSA applications, including electricity generation. These include the Otway Basin (South Australia, Victoria), the Gippsland Basin (Victoria), the Perth Basin (Western Australia), the northern and southern Carnarvon basins (Western Australia) and the Great Artesian Basin (GAB; Queensland, New South Wales, South Australia and the Northern Territory).

Deep, high-temperature HSA resources have been tested in two locations: in the Otway Basin (Panax Geothermal Pty Ltd’s Salamander 1 well); and in the Cooper Basin (Geodynamics Pty Ltd’s Celsius 1 well). Both wells measured high temperatures, but neither achieved sufficient water flow rates (Budd and Gerner, 2015). Research indicated that careful mapping could identify where conditions of poor flow are less likely to occur (South Australian Centre for Geothermal Energy Research, 2014), but no drilling has been conducted to test the research findings. It can be concluded that deep HSA reservoirs have not been adequately tested in Australia.

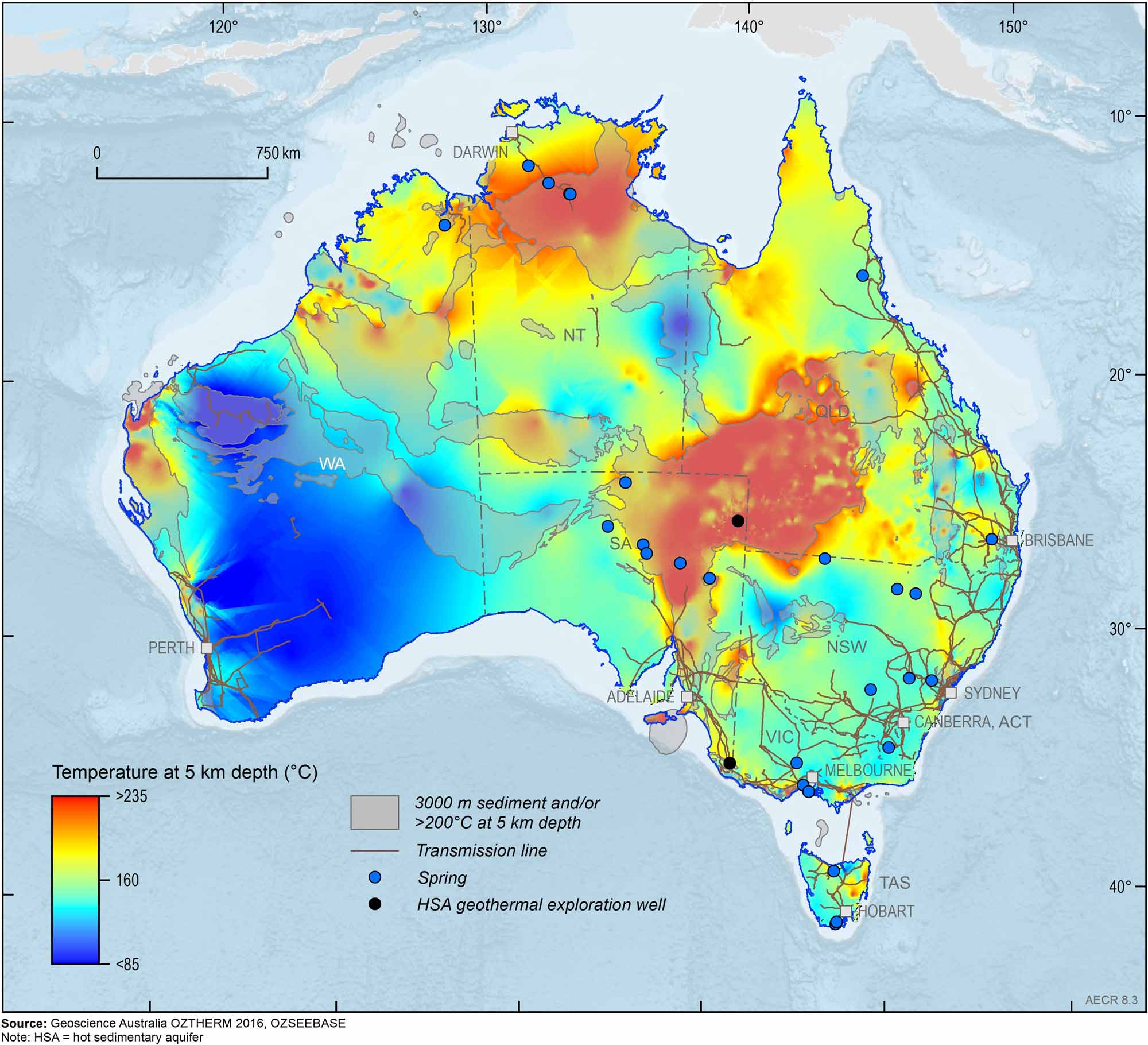

Hot springs are the surface manifestation of an HSA resource (Figure 8.3). They are primarily used for bathing or hydronic heating in Australia. Australian hot springs are typically cooler than parts of the world with higher geothermal gradients, with temperatures generally not exceeding 50°C.

Figure 8.3. Predicted temperature at 5 km depth, showing HSA exploration wells, hot spring locations and areas with >3 km sediment depth and/or temperature of >200°C at 5 km depth.

Enhanced geothermal system (EGS) resources

Data compilations of predicted temperature at 5 km depth suggest that there are substantial areas on the Australian continent where temperatures exceed 200°C at this depth. This is considered the required temperature for geothermal electricity generation to be technically feasible (Figure 8.3). Australia therefore has the potential to contain world-class unconventional geothermal energy resources (Budd et al., 2008).

Deep, high-temperature EGS resources have been tested and hydraulically stimulated in two locations. In the Cooper Basin, Geodynamics Pty Ltd developed the Habanero project (see below); and east of the Flinders Ranges, Petratherm Pty Ltd drilled Paralana 2. The Paralana project was not completed, as sufficient funds were unavailable for the drilling of a second well into the fractured reservoir. It can be concluded that deep EGS reservoirs are yet to be adequately tested in Australia. However, significant technical developments overseas with EGS suggests that the technology may yet hold significant potential for Australia.

Geoexchange and other heat exchange resources

In geoexchange systems (also known as GSHPs), the Earth acts as a heat source or a heat sink, exploiting the temperature difference between the subsurface and atmosphere. The temperature of the Earth just a few metres below the surface is much more consistent than atmospheric temperature, especially in seasonal climates. These resources do not require the addition of geothermal heat, and are perhaps better described as improving energy efficiency (up to 50% in comparison with the commonly used air-sourced heat pumps).

To utilise these stable subsurface temperatures, water or another fluid is pumped through pipes into the ground to change the temperature of the circulating fluid. The optimal-temperature fluid is transported back to the surface to a heat exchanger (water–air loop, such as a reverse-cycle air-conditioning system). In some cases, groundwater is used (i.e. an open system) rather than a closed-loop pipe system.

Other substrates can also be used as heat exchangers, including water bodies or waste products. Examples of systems in use are the Sydney Opera House (using Sydney Harbour as a water-loop heat exchanger) and Sandown Village in Tasmania (using stored effluent as a heat exchanger).

These systems can be installed anywhere in Australia—however there is an economic limitation because installations must be sized to match the building’s heating and cooling load with the available thermal difference between the atmosphere and the ground or other heat sink/source.

World resources

World resources

Geothermal resources globally are widespread and complex, with many different types of systems. Global geothermal resource estimates of the accessible electrical potential range from 35 gigawatts (GW) to 200 GW (World Energy Council, 2016).

Most of the world’s high-temperature geothermal fields (>180°C) are convective hydrothermal systems with a magmatic heat source. These igneous systems include vapour (steam)-dominated fields, such as Kamojang (Indonesia) and Larderello (Italy), as well as liquid-dominated reservoirs that are prevalent in New Zealand, Iceland, Kenya, the Philippines and Japan. Intermediate-temperature resources (101–180°C) associated with convective geothermal systems resulting from high rates of crustal extension include the Basin and Range province in the western United States, and Western Anatolia in Turkey (World Energy Council, 2016).

Conductive systems, where relatively high heat flow and insulation combine to create anomalously hot rock, typically provide low-temperature (30–100°C) to intermediate-temperature geothermal resources. In other configurations (HSAs), conductive heat may be transferred to circulating groundwater, creating artesian warm springs such as Bath (Great Britain) or regional aquifers such as the Malm Limestone in Europe. In rapidly subsiding sedimentary basins, over-pressured mudstones caused by rapid sedimentation may create thermal blankets that trap conductive heat in strata (geopressured aquifers), such as the East Java (Porong) Sub-basin in Indonesia (World Energy Council, 2016).

Australian Capacity

Australian Capacity

Electricity generation

No Australian geothermal electricity generation facilities were active in 2023 but a number of small projects have been trialled over the last decade. The most recent was a small-scale (310 kW) HSA Organic Rankine Cycle geothermal power station which commenced operations in Winton, Queensland, in October 2019 (ThinkGeoEnergy, 2019). The Winton geothermal power plant used hot water from bores drilled into GAB aquifers to generate electricity. The town water supply is GAB bore water, which must be cooled before it is reticulated to users. Rather than waste the heat energy contained by the water, the geothermal power plant used the heat to generate electricity for the town, without affecting the town water supply (Local Government Infrastructure Services, 2016). The power plant is currently inactive due to a legal dispute between the council and project manager (Beardsmore et al., 2023).

Some hope remains that small scale geothermal power plants can be developed in regional Queensland and more broadly, as evidenced by increased activity recently. Greenvale Energy Limited in collaboration with CeraPhi Energy are assessing the potentional for geothermal power generation at Greenvale’s Longreach tenement in Queensland (ThinkGeoEnergy, 2023b). Within Energy has also increased its geothermal portfolio with the addition of three new tenements in Queensland (ThinkGeoEnergy, 2022).

In Western Australia, Strike Energy is also advancing an HSA geothermal prospect with an estimated inferred resource of over 200MWe (mid-case) located 300 km north of Perth, within the Permian Kingia Sandstone, where temperatures in excess of 160 °C have been identified at depths of ~4000 m (Strike Energy, 2022; Ballesteros et al., 2020).

Three geothermal energy projects which previously generated geothermal electricity in Australia, have been decommissioned. The Mulka Station used a hot artesian bore penetrating the Great Artesian Basin to produce a maximum 0.02 MW of electricity in 1986, but was decommissioned three and a half years later after the working fluid for the binary power plant was banned (Burns et al., 2000). The Habanero (Innamincka Deeps) Project was a pilot 1 MW plant, which generated from an EGS resource for five months in 2013 (Geodynamics, 2014). The pilot plant was decommissioned due to insufficient electricity demand in the remote Innamincka area. Finally, from 1992–2017 Ergon Energy operated a low temperature geothermal power station at Birdsville, which sourced hot (98°C) waters at relatively shallow depths from the GAB. Operations were discontinued in 2017 when the plant reached the end of its life. Ergon Energy decided in favour of solar PV and battery systems to replace the geothermal component of the town’s electricity supply, due to the continued reduction in solar technology and energy storage costs (ThinkGeoEnergy, 2018).

Direct-use technologies

According to Beardsmore et al. (2023), the past few years have seen solid growth in terms of direct use geothermal in Australia, both with and without heat pumps. Large-scale direct-use HSA systems, such as those used to heat swimming pools or provide hydronic heating systems and commercial-scale geoexchange systems, are steadily increasing in number in Australia.

Established and effective examples of direct-use geothermal systems include Robarra (Robe, South Australia) and Mainstream Aquaculture (Werribee, Victoria), both growing barramundi using 28–29°C bore water. Midfield Meats (Warrnambool, Victoria), uses warm bore water (boosted to 82°C) for washing and sterilising its industrial meat processing facility. The use of geoexchange technology at scale in housing developments and other large commercial applications has become increasingly common. The Geoscience Australia building in Canberra, the Fairwater Estate GSHP system, and the 72 MWth (megawatts thermal) Barangaroo water-loop heat rejection cooling system are examples.

Since the 2018 AGA census was completed and previous country updates published (Beardsmore et al., 2015, 2021), a number of new direct use projects have been announced or proceeded to implementation (Beardsmore et al., 2023). Large leisure centres in Western Australia implementing geothermal heating have been a common occurrence, with five projects having had recent workovers to maintain injectivity. For example, in 2022, The Craigie Leisure Centre underwent a refurbishment to its geothermal system, which was commissioned in 2005. Finally, in 2021, the Latrobe City Council approved a 2.3 MWth heating system for the Gippsland Regional Aquatic Centre.

In 2022, the Victoria Government awarded a $380,000 grant to the University of Melbourne to design a geothermal heating loop for an industrial zone in the Latrobe Valley, Gippsland (ThinkGeoEnergy, 2023c). The loop system will be designed to deliver heat for end users such as greenhouses, microbrewery, food processing, an onsen, and aquafarms. The region hosts a world class geothermal resource at shallow depths (68°C at 550 to 650 m depth), which has led to significant working interest between the University of Melbourne and industrial partners (Beardsmore et al., 2023).

In recent years, several significant GSHP projects have come into the planning stage, or are in development. Recently, the Fairwater geothermal project was completed, which will provide heating and cooling to 750 homes in New South Wales. An efficiency analysis found that the homes use 21% less electricity than comparable nearby suburbs. Another high profile GSHP project is the Australian War Memorial in Canberra, which started construction in early 2023. This project involves 216 vertical boreholes drilled to a depth of 148 m (Beardsmore et al., 2023). Other projects of note are the Arthur Boyd National Gallery and the Plumbing Industry Climate Action Centre.

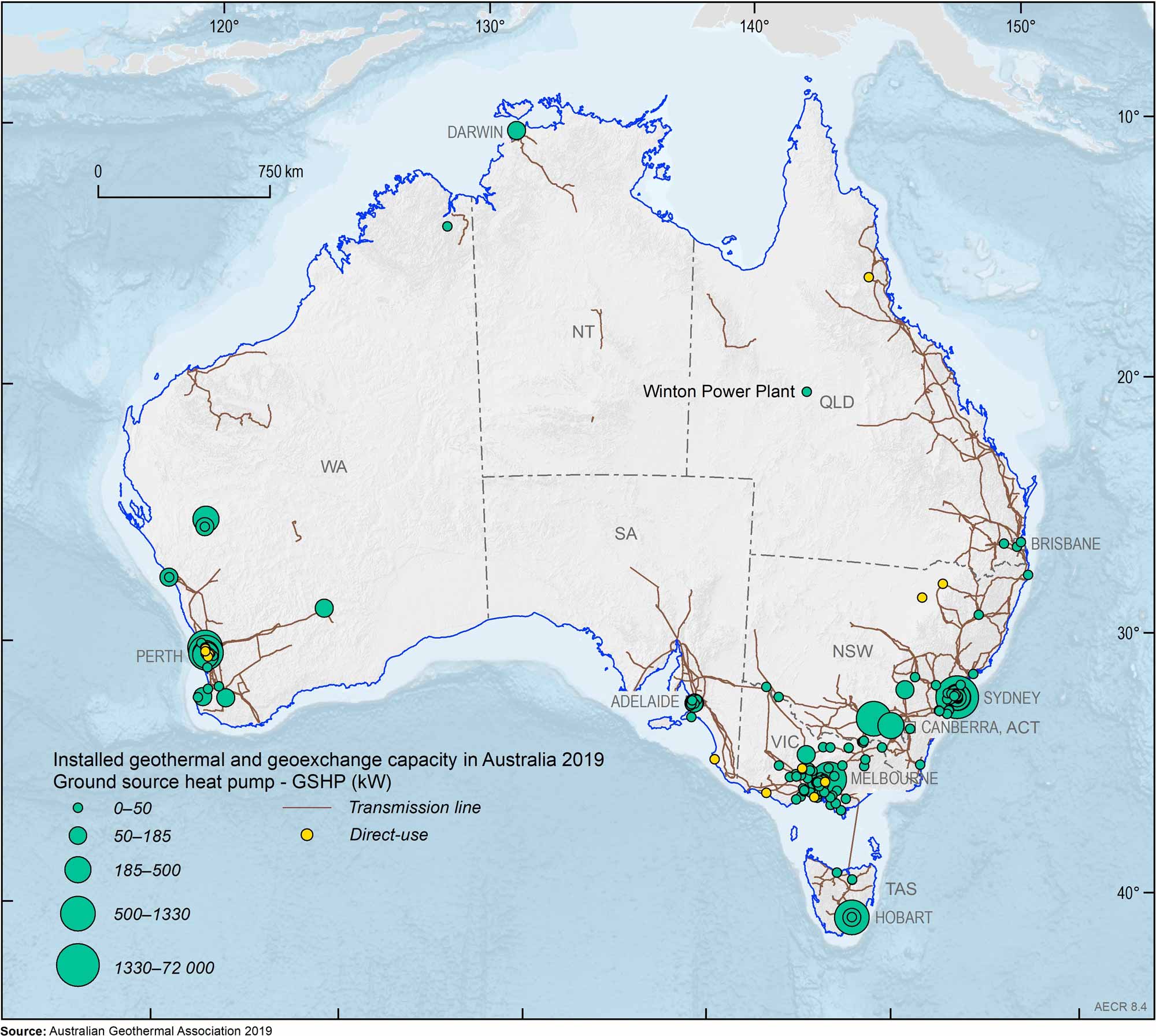

The Australian Geothermal Association has provided data on the installed capacity of direct-use geothermal and geoexchange systems in Australia, including large-scale GSHP and HSA applications through to December 2018 (Figure 8.4). Assuming whichever is the greater of heating or cooling system capacity, Australia has an estimated 29 MWth of direct-use geothermal capacity that is either installed or in the final stages of commissioning, and an additional 105 MWth of total geoexchange capacity. Most of the geoexchange capacity is located in New South Wales, while the bulk of the direct use capacity is in Western Australia and Victoria.

As of January 2023, over 36 MWt of installed capacity for direct use of geothermal heat from hot aquifers has been identified (Beardsmore et al., 2023), an increase of 3 MWt (9%) since 2020. Ground source heat pump capacity is estimated to be 71 MWt, an increase of 9 MWt (14.5%) since 2020.

Figure 8.4. Installed geothermal and geoexchange capacity in Australia during 2019, including ground source heat pump (GSHP) capacity. The Winton Power Plant was a hot sedimentary aquifer (HSA) geothermal power station, which is not currently operational.

Production and consumption

Production and consumption

No geothermal electricity was generated in Australia in 2022-23. In 2016–17, 0.5 gigawatt hours (GWh) of electricity was generated from geothermal sources, accounting for only a very small share of the country's total renewable generation. The Birdsville power plant ceased supplying its customers with geothermal power in 2017, with Ergon opting instead to pursue a solar PV and storage strategy (ThinkGeoEnergy.com, 2018).

The world’s installed geothermal capacity has been growing over the past decade, reaching 14.8 GW in 2023 (International Renewable Energy Agency, 2024). In 2021, global geothermal power plants produced approximately 95 TWh of electricity which was about 0.33% of the world’s electricity generation. Geographically, 72% of installed generation capacity resides along tectonic plate boundaries or ‘hot spot’ features of the Pacific Rim (World Energy Council, 2016). All of these are igneous convective resources. In contrast, only 20% of total installed generation capacity resides in convection fields situated along spreading centres and convergent margins within the Atlantic Basin. A disproportionate percentage of installed generation capacity globally resides in island nations or regions (43%). Virtually all these resources occupy positions either at the junction of tectonic plates (such as Iceland) or within a ‘hot spot’ (e.g. Hawaii; World Energy Council, 2016). Technological improvements have made it possible for most countries to use shallow low-temperature geothermal resources in addition to higher-temperature resources, and these opportunities are expanding rapidly.

Australia is significantly lagging behind the top ten geothermal electricity–generating countries (Table 8.1). In 2021, Australia was ranked 41st in the world in direct-use geothermal utilisation (Lund and Toth, 2021), which is up from 57th in the previous assessment (Lund and Boyd, 2016). Australia’s use of geothermal energy is insignificant when compared to that of the world leader, China (Table 8.2).

Table 8.1. Top ten countries for installed geothermal electricity generation capacity, and Australia, end 2022.

| Country | 2022 MWe |

|---|---|

| United States | 3,794 |

| Indonesia | 2,356 |

| Philippines | 1,935 |

| Turkey | 1,682 |

| New Zealand | 1,037 |

| Mexico | 963 |

| Kenya | 944 |

| Italy | 944 |

| Iceland | 754 |

| Japan | 621 |

| Other | 1,097 |

| Australia | - |

Abbreviations

MWe = megawatts electrical

Notes

Source: ThinkGeoEnergy, 2023a

Table 8.2 Selected world direct-use geothermal utilisation, 2021.

| Rank | Country | Installed capacity (MWth) | Energy consumption (TJ/year) |

|---|---|---|---|

| 1 | China | 40,610 | 443,492 |

| 2 | United States | 20,713 | 152,810 |

| 3 | Sweden | 6,680 | 62,400 |

| 4 | Turkey | 4,806 | 29,139 |

| 5 | Germany | 3,488 | 54,584 |

| 41 | Australia | 94 | 853 |

Abbreviations

MWth = Megawatts thermal; TJ = Terajoules.

Notes

Source: Lund and Toth, 2021.

Outlook

Outlook

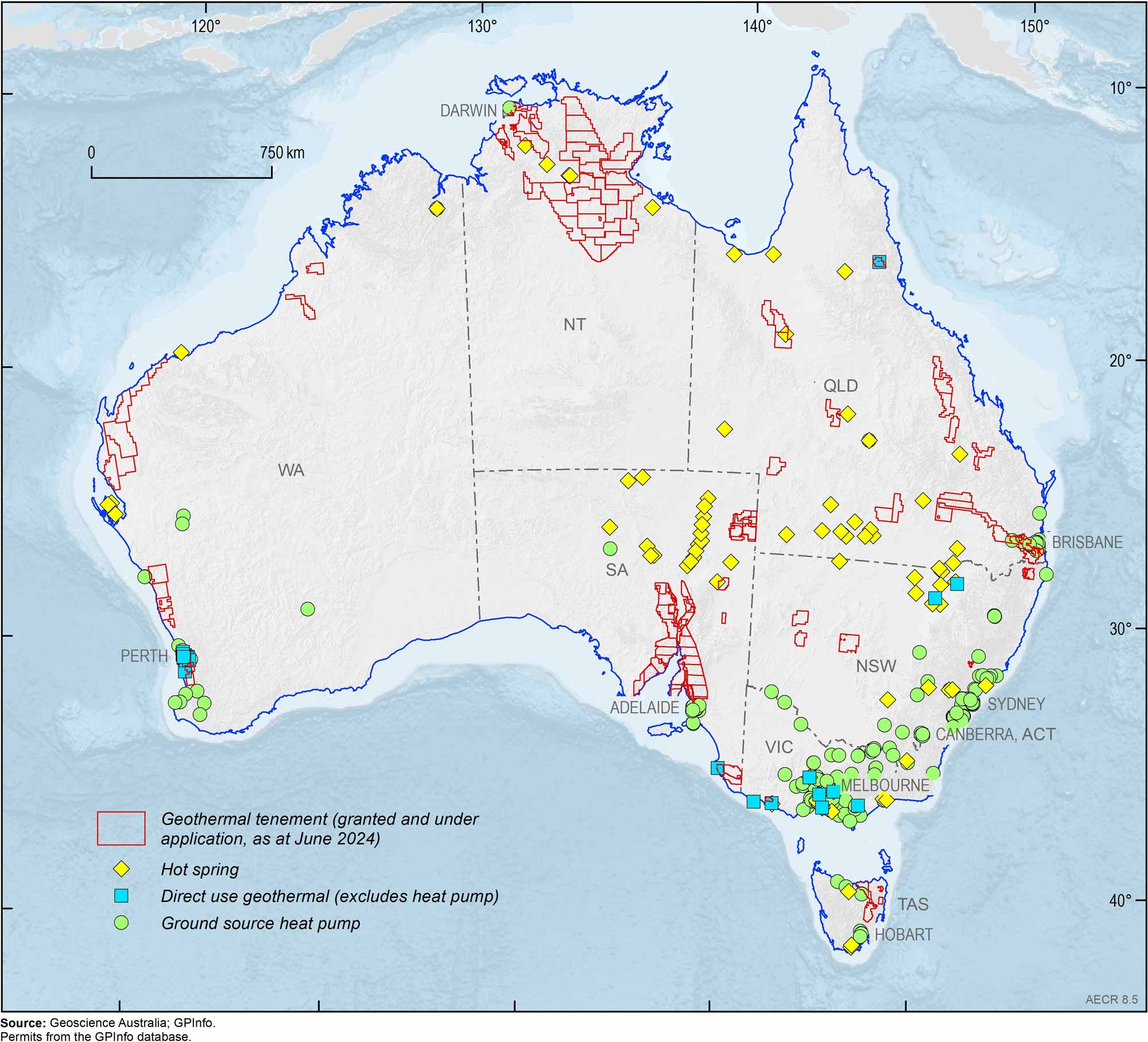

Geothermal energy has a number of appealing attributes for addressing Australia’s future energy requirements. In particular, unlike most renewable technologies, geothermal energy is not variable over time and does not require energy storage. In the past few years there has been a renewed surge of interest in geothermal energy in Australia, as evidenced by the large take-up of geothermal tenements across the country (Figure 8.5 and Beardsmore et al., 2023).

In Australia, installations exploiting shallower and lower-temperature HSA geothermal and geoexchange resources are increasing in number. Ground source heat pumps and other direct-use or geoexchange technologies have been installed without any financial assistance from the government and they will act as energy consumption offsets (i.e. do not provide electricity but reduce electricity or gas consumption). Large projects such as Fairwater Estate may help to lower future installation costs of these systems by establishing a supply chain, including installation and maintenance skills and experience.

Although geothermal energy has until now been unsuccessful as a power generation source in Australia, there have been significant technological advances internationally which hold much promise for the future. Recently, Fervo Energy successfully utilized multi-stage reservoir stimulation techniques to create an EGS with much higher flow rates than have been achieved previously and estimate that one producer/injector pair can sustain a 3.5 MW power plant at their location (ThinkGeoEnergy, 2023d). The success of the technology hinges on the drilling of cased horizontal wells with multiple perforations, which allows much larger volumes of rock to be tapped for heat.

Advanced Geothermal Systems (AGS) also hold much potential for electricity generation and are very much in the early stages of development. AGS is different to EGS in that they are closed loop systems that do not involve fluids penetrating into the rock from one well to another. The technology works similarly to a GSHP except under hotter conditions and involving significantly longer wellbores (Department of Energy, 2024). Perhaps the most notable closed loop geothermal project is the Eavor Technologies demonstration project in Germany. The project involves four loops drilled to approximately 4–5 km depth, and is estimated to produce 8 MW of power in 2027. Projects such as these hold much promise that EGS and AGS will successfully be deployed in Australia in the near future.

Figure 8.5. Map of Australian geothermal projects and current geothermal tenements.

Factors influencing development

Geothermal resources are used in situ; hot water cannot be piped far without losing heat. Powerlines, on the other hand, can carry electricity significant distances with low line losses. Therefore, additional transmission lines must be built if transmission infrastructure does not exist where the geothermal resource is located. Mapping of geothermal resources and matching them to a potential energy use (e.g. direct use, electricity on- or off-grid) is an important precursor to development. Doing this effectively is a key component of reducing investment risk and costs.

Systems using geothermal energy for heating and cooling to displace electricity or gas have been demonstrated to be cost competitive (e.g. GSHPs, swimming pool heating). Geoexchange systems are more energy efficient than air-source heat pumps, which offsets the higher installation costs (Lu et al., 2017). In contrast, the geothermal electricity generation sector is at an immature stage of development. Currently, initial pre-survey exploration and test drilling stages in the life cycle of a geothermal project contain high project risks and potential costs. The risks and associated costs will be mitigated by improved geological understanding of how these resources work, and improved technology for exploration and drilling. In the life cycle of a geothermal project, costs typically rise significantly after the feasibility studies have been completed. Upfront costs, for well drilling and plant construction, are the biggest contributors to the overall capital costs of geothermal energy generation, depending on the technology. Improving technologies for energy conversion, including for power plant cooling in arid terrains, will reduce these costs.

Improving the efficiency of energy conversion of geothermal resources (for both electricity generation and direct-use applications) directly affects the cost of installation (i.e. smaller plant for same output) or the size of the available resource base (i.e. lower-temperature resources can be used commercially). In the near term, improvements in energy efficiency could allow the exploitation of shallower—and hence less expensive—HSA electricity generation possibilities and improve the cost effectiveness of direct-use applications. Technology improvements affecting conversion efficiency include improved turbines and power plant cooling systems.

Finally, it is recognised that community consultation will be an important part of any future deep EGS geothermal projects in Australia as development of deep EGS electricity projects will require drilling and hydraulic stimulation activities.

References

References

Australian Geothermal Association, 2019. Census of Geothermal Projects. (Last accessed 29 April 2024).

Australian Renewable Energy Agency, 2014. Looking Forward: Barriers, Risks and Rewards of the Australian Geothermal Sector to 2020 and 2030. Commonwealth of Australia.

Ayling, B.F., Budd, A.R., Holgate, F.L. and Gerner, E., 2007. Direct use of geothermal energy: opportunities for Australia, fact sheet. Geoscience Australia, Canberra.

Ballesteros, M, Pujol, M., Aymard, D. and Marshall, R., 2020. Hot sedimentary aquifer geothermal resource potential of the Early Permian Kingia Sandstone, North Perth Basin, Western Australia. Geothermal Resources Council Transactions, 44, 477–503.

Beardsmore, G., Budd, A. R., Huddlestone-Holmes, C. and Davidson, C. 2015. Country update – Australia. In: Proceedings of the World Geothermal Congress, Melbourne, Australia, 19–25 April 2015.

Beardsmore, G., Davidson, C., Payne, D., Pujol, M., and Ricard, L., 2021. Australia – Country Update, Proceedings, World Geothermal Congress, 2020+1, Reykjavik, Iceland, (April–October, 2021).

Beardsmore, G., Ballesteros, M., Davidson, C., Larking, A., Pujol, M., 2023. Australia – Country Update, Proceedings, World Geothermal Congress 2023, Beijing, China (October 8-13, 2023)

Budd A. R. and Gerner, E. J. 2015. Externalities are the dominant cause of faltering in Australian geothermal energy development. In: Proceedings of the World Geothermal Congress, Melbourne, 19–25 April 2015 (last accessed 18 February 2020).

Budd, A. R., Holgate, F. L., Gerner, E., Ayling, B. F. and Barnicoat, A., 2008. Pre-competitive geoscience for geothermal exploration and development in Australia: Geoscience Australia’s Onshore Energy Security Program and the Geothermal Energy Project. In: Proceedings of the Sir Mark Oliphant International Frontiers of Science Australian Geothermal Energy Conference, Gurgenci, H. and Budd, A.R. (eds), Record 2008/18, Geoscience Australia, Canberra,1–8.

Burns, K. L., Weber, C., Perry, J. and Harrington, H. J., 2000. Status of the geothermal industry in Australia. In: Proceedings of the World Geothermal Congress 2000, Kyushu–Tokohu, Japan, 28 May –10 June 2000, 99–108.

Department of Climate Change, Energy, the Environment and Water, 2023. Australian Energy Statistics (Last accessed 29 April 2024).

Department of Energy, USA, 2024. Pathways to Commercial Liftoff: Next-Generation Geothermal Power (last accessed May 22, 2024)

Geodynamics Pty Ltd, 2014. Habanero Geothermal Project Field Development Plan, 9 October 2014. (Last accessed 29 April 2024).

International Renewable Energy Agency (IEA). 2024. Energy Transition Technology: Geothermal Energy (Last accessed 18 April 2024).

Local Government Infrastructure Services, 2016. Submission to the Queensland Renewable Energy Expert Panel issues paper.

Lund, J. W. and Boyd, T. L., 2016. Direct utilization of geothermal energy 2015 worldwide review. Geothermics, 60, 66–93.

Lund, J. W., Toth, A. N., 2021. Direct Utilization of Geothermal Energy 2020 Worldwide Review, Proceedings World Geothermal Congress 2020+1, Reykjavik, Iceland, April - October 2021

South Australia Centre for Geothermal Energy Research, 2014. Program 2 Summary Report, ARENA Measure: Reservoir quality in sedimentary geothermal resources (last accessed 22 April 2024).

Strike Energy Limited, 2022. Mid-West Geothermal Power Project Inferred Resource Statement, announcement to the Australian Securities Exchange, (5 May 2022), 5 pp. (Last accessed 22 April 2024).

ThinkGeoEnergy. 2018. Birdsville in Australia abandons plans for renewal of geothermal plant (last accessed 15 April 2024)

ThinkGeoEnergy. 2019. 310 kW Winton geothermal power plant in Queensland, Australia starts operation (last accessed 15 April 2024).

ThinkGeoEnergy, 2022. Within Energy acquires new geothermal exploration permits in Queenslands, Australia

ThinkGeoEnergy. 2023a. Latest top 10 list of geothermal countries - Year-End 2022 (power generation capacity) (last accessed 15 April 2024).

ThinkGeoEnergy,2023b. CeraPhi and Greenvale complete geothermal study in Longreach, Australia (last accessed 22 April 2024).

ThinkGeoEnergy, 2023c. University of Melbourne receives funding for geothermal heating loop design (last accessed 22 April 2024)

ThinkGeoEnergy, 2023d Fervo Energy reports breakthrough in field-scale EGS project in Nevada (last accessed May 23, 2024).

World Energy Council. 2016. World Energy Resource, Geothermal 2016 (last accessed 16 April 2024).

Data download

Data download

Australia's Energy Commodity Resources Data Tables - 2022 reporting period